Fri, 27 December 2013

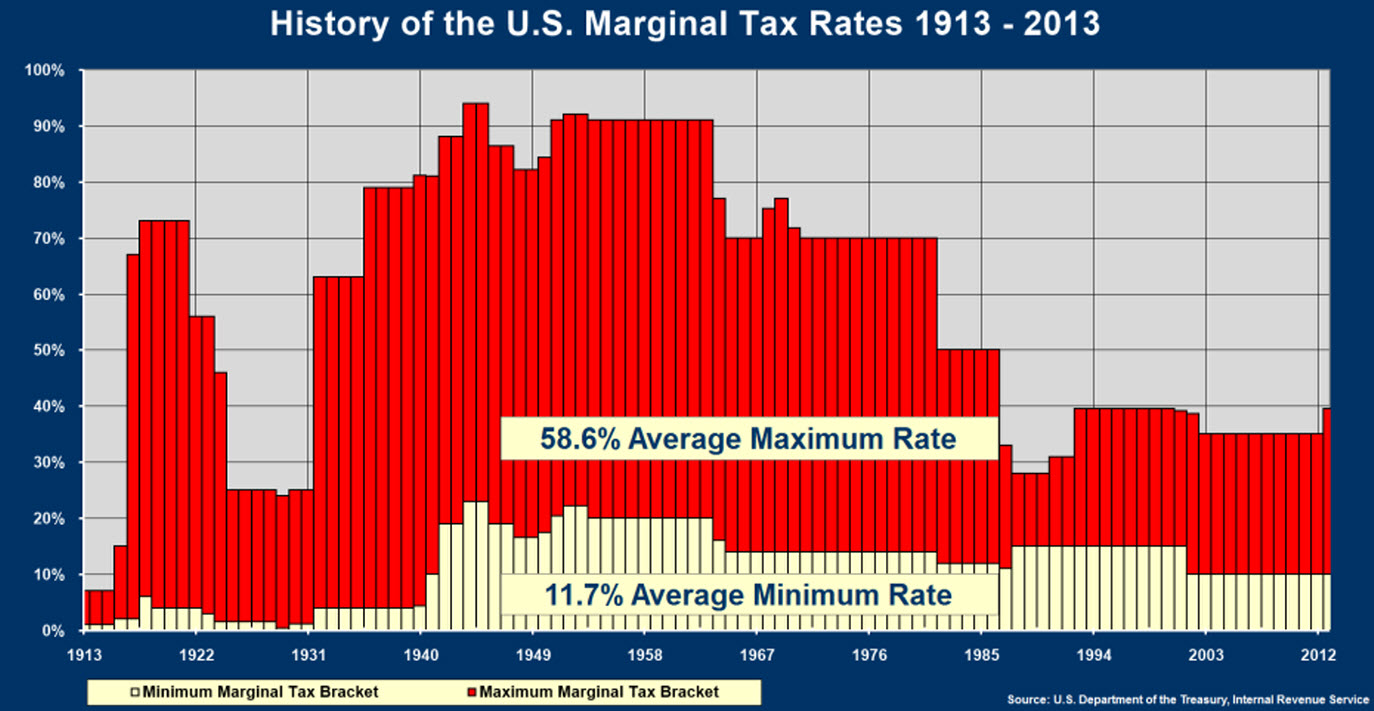

LOOK WHAT THE WEALTHY ARE DOING Remember to access this week's video and all other links by going to "Extras" from within your David Lukas Show App. This is a continuation from last week's show: Look What The Banks Are Doing Be sure and watch this weeks video below. You don't want to miss it! Why is this show titled "Look What The Wealthy Are Doing"? Because, under the current IRS tax code, a properly structured cash value life insurance policy, is one of the few assets that provide tax-advantaged access (I.E. Tax-Free Distribution). In fact, when setup properly, they are treated and taxed exactly like a ROTH IRA. (Both are governed by IRS code section 7702) . It should be noted that many agents do not understand how to setup a policy in this fashion. You should be 100% certain you are working with someone that is an expert in this area. When the right policy is put in place, not only are the proceeds tax-free, but there are much higher contribution limits when compared to ROTH IRAs. (Many people fund these plans at $60,000 per year or more. Compare this to the limitations of ROTH IRA's and the fact that many high income earners can't event participate in a ROTH IRA. See the entire list of benefits HERE (Also watch the video below) Watch the video below to see David give a detailed analysis Of a Cash Value Life Insurance Policy VS. an alternative market based account. (From within your App, click on "Extras" and the hit "Play Bonus Content". There is a lot of negative information out there about cash value life insurance. Much of it is based on a misunderstanding of how these policies work . In fact, many life insurance agents don't even know how to setup a policy to maximize the living benefits that a contract offers. Additional Resources to learn more: SEE: Look What The Banks Are Doing 10MinuteLessonOnLifeInsurance.com Also see the video: Borrowing Strategies. David and his firm specialize in these advanced insurance strategies and can assist you further on this topic. David and his team can be reached at: (800) 559-0933 or visit: InfiniteFinancialServices.com As David promised on this broadcast, we've included Federal Income tax rate history since its inception in 1913. (See Extras to view Federal Income Tax History)

|

Thu, 26 December 2013

Look What The Banks Are Doing, Not What They Want You To Do. As always, if you are reading this from your Smart Phone App, go to "Extras" to access any of the links that are mentioned below. If you haven't done so yet, be sure to check out the following broadcast: Think and Operate Like a Bank and How Banks Make Money This week David talks about one an asset that banks hold billions and dollars of dollars in. In fact, in a recent period, banks bought up over 40-billion dollars in this asset. What is it you may ask? Banks own billions of Dollars in BOLI's (Banked Owned Life Insurance). The largest banks currently own up to 25% of their safest assets (Tier-One Capital) in Cash Value Life insurance. It's very telling when you study the balance sheets of the very financial institutions who advocate that the average investor on main street speculate with their life's savings while they in fact do the exact opposite. For instance, in a recent 9-month period, Citibank bought up over 1-billion dollars in Cash Value Life Insurance to add to their investment holdings. During this same time period, do you know what Citibank's wholly owned subsidiary was advising their clients when visiting their website? "Buy Term and Invest The Rest" (speculate). This is only one of many examples of the hypocrisy that exist by the Big Banks who own the Major Wall Street firms. Much of this information can be validated by the research of our good friend Barry Dyke and his book: The Pirates Of Manhattan. An industry doesn't buy over 40-billion dollars of something that is bad for them during during a shaky economy. David mentions a few of his recent Show: You Can't Spend Average, The Great Wall Street Retirement Scam David extensively talks about a Forbes Article: The Real Cost of Owning Mutual Funds Stop and read this article. It's well worth it if you have every owned a mutual fund. Stay tuned, next week, David is going to break down the numbers behind properly structured cash value policy vs. an alternative market-based investment and how it would realistically performed in comparison to an actual cash value policy. Study the facts and get informed. Those who would have you believe that a cash value policy has no place in your life have ulterior motives. Don't just listen to Wall Street and wand what their advisors are advocating. Studying what they do is more revealing of the truth. Wall Street does NOT want informed people capable of critical thinking to make important financial decisions with regard to their savings. Don't just take our word for it, do your own research. Listen in to find out why what you thought to be true about Life insurance is not true. It's not just about the death benefits. When you work with someone who understands how to properly structure an over-funded cash value policy, you will come to realize like the banks have that this is one of the most powerful asset classes that can help you weather the upcoming financial storms. Till Next week, you can go to: 10MinuteLessonOnLifeInsurance.com Also See: An Economic WorkHorse

|

Sat, 14 December 2013

Who won the game of tic tac toe the first time you played? You and I regularly lost this game as children until we understood the rules and strategy of the game. Do the financial institutions teach you the rules? NO! They aren’t about to tell you how to play the game. When you learn the rules and strategies of winning the game, only then will you turn the banking equation in your favor. Who controls the banking equation in your life? If you don’t control the banking equation, by default, the banks will happily fill this roll. The average American pays 34.5% of their income to someone else’s bank. Seemingly the solution to this problem is to pay cash for everything. This common mind set seriously hinders people’s ability to accumulate substantial long term savings. They’ve unknowingly failed to maximize what Albert Einstein said was the eighth wonder of the world: Compounding Interest. SEE: Why Compounding Interest Doesn’t Work. at the following link: https://dlshowonline.com/why-compound-interest-doesnt-work/ or Access this show by clicking on "Extras" from within this app. Paying cash for life’s major purchases seemingly is a wise financial choice. However, this notion overlooks the fact that We Finance EVERYTHING We buy. We either pay interest, or We give up the ability to earn interest. Banking is one of the most profitable businesses in the world. (See recent broadcast: How Banks Make Money here: https://dlshowonline.com/how-banks-make-money/ Be sure to watch the video, Access this show by clicking on "Extras" from within this app. It’s time you begin to think and operate like a bank, or you will be perpetually enslaved to a system built to keep you coming back for more. Watch the video below to understand various banking strategies. What is the most efficient way to go about making life’s major purchases such as automobiles? David, breaks down the math and analyzes multiple borrowing strategies. Always remember: The way you spend your money is equally important as the act of actually saving your money.There are two links in the video that you should be able to click on from within the video. Our apologies, there’s a technical glitch and that’s being worked on. |

Sat, 7 December 2013

This week David talks about the importance of understanding why much of the prevalent mindset of achieving retirements savings objectives is often synonymous with taking on more risk. The greatest definition of Risk is the likelihood of loss. Most people mistakenly associate risk (related to their retirement savings) with the probability that they will "hit it out of the park" or "win big" by experiencing higher rates of return. The true definition of risk is the likelihood of loss. Let's think through this logic for a moment.... You have to take on more chance of losing everything, so you can get more money and get ahead? Logically does this make sense? Yet, this is sold to the American public by way most "Financial Advisers" promoting common strategies propagated by Wall Street. Listen to David explain the real problem behind why many individuals fails to meet their long-term financial objectives. The answer is not found in chasing higher rates of return and subsequently taking on more risk of loss. The answer, is more simple than you think. Be sure and watch the accompanying video as David validates these ideas with math. You can watch this video from your Official David Lukas Show Smart Phone app by going to "Extras" and clicking on "Play Bonus Content" |

The David Lukas Show

Categories

generalFederal Budget

Archives

FebruarySeptember

August

July

June

April

March

February

January

November

October

September

August

June

March

February

January

December

November

October

September

July

June

May

April

March

February

January

December

November

October

September

August

July

June

May

April

March

February

January

October

September

August

July

June

April

March

February

January

December

November

October

September

August

July

June

May

April

March

February

January

December

November

October

September

August

July

June

May

April

March

February

January

December

November

October

September

August

July

June

May

April

March

February

January

December

November

October

August

July

June

May

April

March

February

January

December

November

October

September

August

July

June

May

April

March

February

January

December

November

October

September

August

July

June

May

April

March

June

March

January

| S | M | T | W | T | F | S |

|---|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 | 6 | 7 |

| 8 | 9 | 10 | 11 | 12 | 13 | 14 |

| 15 | 16 | 17 | 18 | 19 | 20 | 21 |

| 22 | 23 | 24 | 25 | 26 | 27 | 28 |

| 29 | 30 | 31 | ||||

Syndication

{kind=link}